It’s March. HR asks you to declare your tax regime for FY 2026–27. Your colleague says, “New regime is better.” Your cousin says, “Old regime saves more with HRA.” You open a calculator. Ten tabs later, you’re more confused.

Let’s fix that.

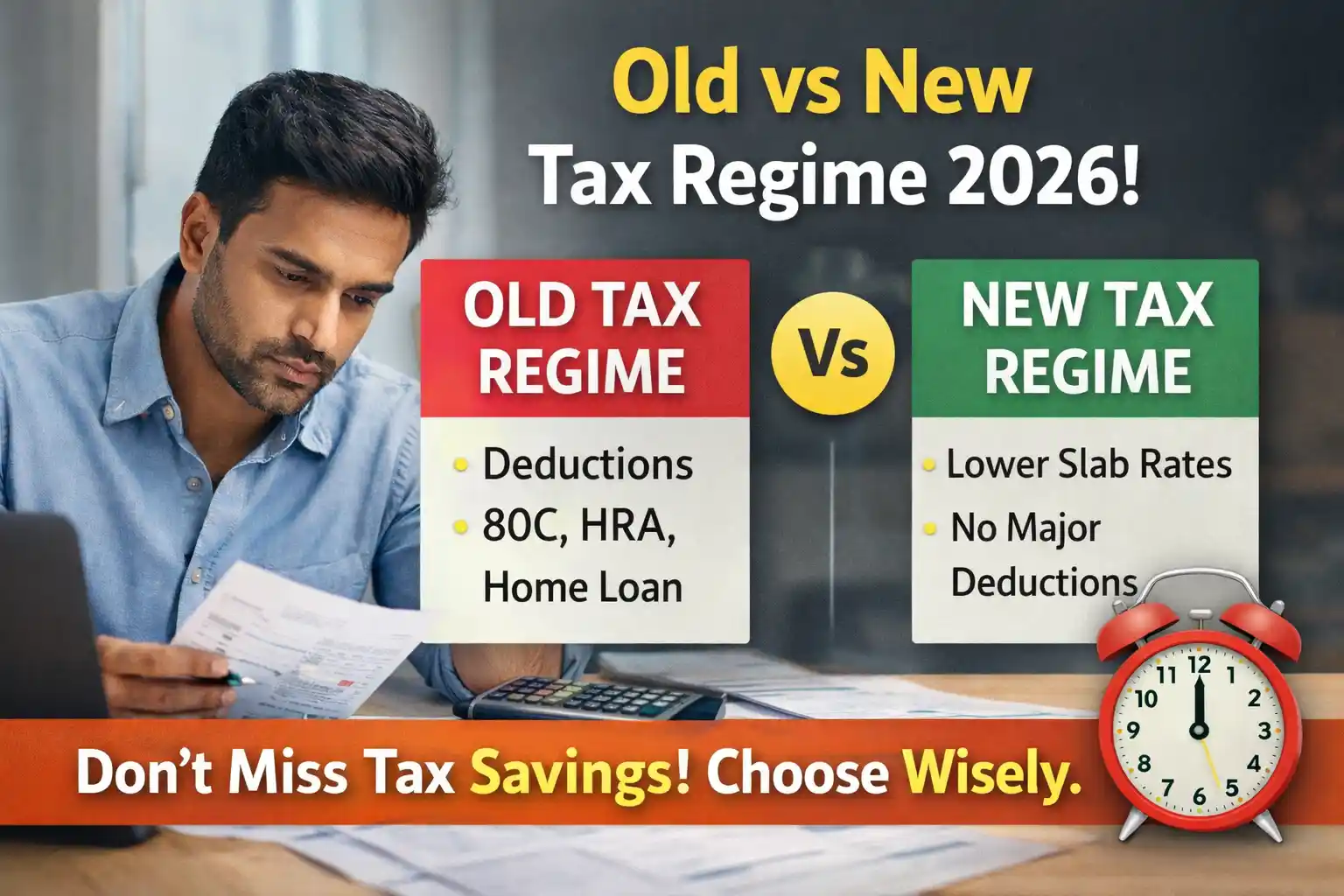

Old vs New Tax Regime 2026

The old tax regime offers lower tax rates only if you claim multiple deductions (HRA, 80C, home loan interest, etc.), while the new regime provides lower slab rates with almost no deductions. Your best choice depends on total deductions—not opinions.

Key Takeaways

- New regime = simpler, fewer deductions, often better for low-to-mid deductions.

- Old regime = beneficial only if total deductions are substantial.

- HRA, 80C, and home loan interest matter only in old regime.

- Regime choice can usually be changed yearly (for salaried individuals).

- The right decision is math-driven, not emotional.

When to Get Professional Help

This is a financial decision. If you:

- Earn above ₹20–25 lakh

- Have ESOPs or capital gains

- Claim multiple deductions

- Run a business or freelance

Consult a qualified CA.

Risk Levels

- Level 1: Salary only, basic deductions.

- Level 2: Home loan + HRA + investments.

- Level 3: Business income or tax notice.

This article is educational—not personalized advice.

What Is the Old Tax Regime?

The old regime follows traditional slabs and allows multiple deductions:

Common Deductions Available

- Section 80C (up to ₹1.5 lakh)

- HRA

- Home loan interest (Section 24)

- Health insurance (80D)

- Education loan interest

- LTA

- Meal benefits (if structured)

It rewards structured financial behavior.

But paperwork matters.

What Is the New Tax Regime?

The new regime offers:

- Lower slab rates

- Almost no deductions

- Standard deduction (if applicable under current rules)

- Cleaner filing experience

It removes complexity.

It also removes flexibility.

Tax Slab Structure (Conceptual Comparison)

(Slabs may change with Budget announcements. Always verify current rates on official Income Tax portal.)

Generally:

- New regime has lower rates in middle slabs.

- Old regime keeps traditional slabs but allows deduction stacking.

The difference appears small—until you apply deductions.

First-Principles Decision Logic

Think in two buckets:

Bucket 1: Gross Income

Bucket 2: Total Deductions

If deductions are low → new regime often wins.

If deductions are high → old regime may win.

There’s no ideological answer. Only arithmetic.

Scenario Analysis (Realistic Comparisons)

Scenario 1: Income ₹7–8 Lakh

Deductions: minimal (₹50,000–₹1 lakh)

New regime usually wins because:

- Lower slab rates

- Rebate eligibility (if applicable)

- Less documentation

Old regime rarely makes sense unless strong deductions exist.

Scenario 2: Income ₹12–15 Lakh

Deductions:

- ₹1.5 lakh 80C

- ₹2 lakh home loan interest

- ₹1.2 lakh HRA

- ₹25,000 health insurance

Now old regime becomes competitive.

But only if you actually qualify for full deduction amounts.

Many assume they do. They don’t.

Scenario 3: Income ₹20–25 Lakh

If deductions exceed ₹4–5 lakh, old regime may reduce tax significantly.

If deductions are below ₹2 lakh, new regime often simplifies life with similar tax outcome.

At higher income levels, marginal slab impact matters more.

HRA: The Deciding Factor for Many

HRA works only in the old regime.

If:

- You live in a metro

- Rent is high relative to salary

- Employer structures HRA

Then old regime gains strength.

If you live in own house or with parents (without proper rent documentation), HRA advantage disappears.

Home Loan Impact

Home loan interest (up to ₹2 lakh for self-occupied property) is a powerful old-regime benefit.

But ask yourself:

Are you paying interest mainly to save tax?

Tax savings rarely justify large interest burdens alone.

80C Reality Check

Many people assume ₹1.5 lakh 80C automatically applies.

It only applies if you invest.

Common 80C instruments:

- EPF

- PPF

- ELSS

- Life insurance premium

- Principal home loan repayment

If you’re not maxing it, old regime loses edge.

Education & Minor Allowances

These provide modest relief.

They rarely tilt the full regime decision.

Avoid overestimating small deductions.

Simplicity vs Optimization

Here’s the trade-off:

| Factor | Old Regime | New Regime |

|---|---|---|

| Paperwork | High | Low |

| Flexibility | High | Low |

| Complexity | Moderate–High | Low |

| Tax predictability | Variable | Stable |

| Best for | Deduction-heavy earners | Low-deduction earners |

Psychological Bias in Regime Choice

Many prefer old regime because:

“I don’t want to lose benefits.”

But if deductions are small, you’re holding onto paperwork for little gain.

New regime often reduces compliance stress.

Time has value too.

Common Misconceptions

Myth 1: New regime is always better

Not true. High deductions still favor old regime.

Myth 2: Old regime gives more refunds

Refund size depends on TDS planning—not regime superiority.

Myth 3: You can’t switch regimes

Salaried individuals can typically choose annually.

Myth 4: HRA alone justifies old regime

Only if it meaningfully reduces taxable income.

Myth 5: New regime removes all deductions

Some limited components may still apply depending on rules.

Decision Helper (IF–THEN Framework)

Choose Smartly

- IF income < ₹7 lakh → Compare rebate carefully; new regime often simpler.

- IF deductions < ₹2 lakh → New regime usually efficient.

- IF deductions > ₹3–4 lakh → Calculate old regime seriously.

- IF you hate paperwork → New regime reduces friction.

- IF you have home loan + HRA + 80C maxed → Old regime likely competitive.

Always calculate both before declaring.

FAQ

1. Which tax regime is better in 2026?

It depends on total deductions versus slab benefits.

2. Can I change regime every year?

Salaried individuals generally can choose annually.

3. Is HRA allowed in new regime?

No, it applies only under old regime.

4. Does new regime remove 80C?

Most deductions under 80C are not available.

5. Which regime gives higher refund?

Refund depends on TDS planning.

6. Is home loan benefit available in new regime?

Typically not for self-occupied property.

7. Is new regime mandatory?

No, choice remains available.

8. Should high earners choose old regime?

Only if deductions are substantial.

10-Minute Action Plan

List all deductions you actually qualify for.

Total them honestly.

Use official tax calculator for both regimes.

Compare final tax payable—not assumptions.

Inform HR before deadline.

Cheat Sheet Summary

| Situation | Likely Better Option |

|---|---|

| No home loan, low investments | New Regime |

| High rent + 80C + home loan | Old Regime |

| Salary under ₹7 lakh | Often New |

| High income, low deductions | New |

| High income, high deductions | Old |

Sources

- Income Tax Department of India – incometax.gov.in

- Ministry of Finance – finmin.nic.in

- Press Information Bureau – pib.gov.in

Last Updated: 13 February 2026